How Banking Sector Works

At its core, the banking industry exists to move money efficiently through the economy. Banks collect savings from individuals and institutions, channel those funds into loans and investments, facilitate payments, and act as custodians of financial trust. This simple idea—intermediating between savers and borrowers—supports consumption, business expansion, and overall economic growth. Modern banking, however, is far more than deposit-taking and lending

4/19/20264 min read

Introduction

At its core, the banking industry exists to move money efficiently through the economy. Banks collect savings from individuals and institutions, channel those funds into loans and investments, facilitate payments, and act as custodians of financial trust. This simple idea—intermediating between savers and borrowers—supports consumption, business expansion, and overall economic growth. Modern banking, however, is far more than deposit-taking and lending; it encompasses risk management, digital payments, treasury operations, compliance, and a dense regulatory framework designed to protect depositors and ensure systemic stability.

A Brief History of Banking

Banking traces its origins to ancient civilizations where merchants extended grain loans and early “bankers” safeguarded valuables. In India, indigenous banking practices such as hundis enabled trade long before formal institutions emerged. The colonial period saw the establishment of presidency banks, which eventually merged to form the Imperial Bank of India, later nationalized and reconstituted as the State Bank of India in 1955.

Post-independence, India witnessed two major waves of bank nationalization (1969 and 1980) aimed at expanding credit access and financial inclusion. The liberalization reforms of 1991 marked a turning point, opening the sector to private participation and competition. New-generation private banks brought technology, customer-centric products, and efficiency, accelerating the modernization of the industry.

How Banks Actually Operate

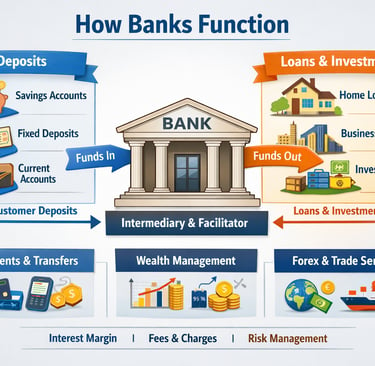

Banks function through a balance sheet model. On the liability side, they mobilize deposits—savings accounts, current accounts, and fixed deposits. On the asset side, they deploy these funds into loans (retail, corporate, MSME) and investments (government securities, bonds). The difference between the interest earned on assets and the interest paid on liabilities is called the net interest margin (NIM), a key driver of profitability.

Beyond lending, banks earn fees from services such as payments, wealth management, distribution of financial products, and trade finance. Risk management sits at the heart of operations: banks must assess borrower creditworthiness, maintain capital buffers, and manage liquidity so they can meet withdrawal demands at all times.

Public vs Private Sector Banks

India’s banking landscape is broadly divided into public sector banks (PSBs) and private sector banks.

Public sector banks, led by institutions like the State Bank of India, are majority-owned by the government. Historically, they have played a critical role in financial inclusion, rural outreach, and priority sector lending. Their strengths include scale, trust, and reach, though they have, at times, grappled with asset quality challenges and operational efficiency.

Private sector banks, including leaders such as HDFC Bank and ICICI Bank, are known for agility, technology adoption, and superior customer experience. They have typically delivered stronger profitability metrics and faster growth, particularly in retail lending and digital banking.

Both segments are essential: PSBs provide breadth and inclusion, while private banks drive innovation and efficiency.

Regulatory Environment and Key Laws

Banking is one of the most tightly regulated sectors in any economy. In India, the Reserve Bank of India (RBI) acts as the central bank and primary regulator. It oversees monetary policy, licensing, supervision, and systemic stability.

Several key laws and frameworks govern the sector:

The Banking Regulation Act, 1949 defines how banks operate and are supervised.

The Reserve Bank of India Act, 1934 establishes the RBI’s powers and responsibilities.

The Insolvency and Bankruptcy Code, 2016 (IBC) provides a time-bound process to resolve stressed assets, improving recovery for lenders.

Prudential norms based on global Basel standards (capital adequacy, liquidity coverage) ensure banks maintain buffers against risks.

Additionally, deposit insurance (through DICGC) protects small depositors up to a specified limit, reinforcing trust in the system.

Growth of the Indian Banking Sector

Over the past two decades, Indian banking has expanded alongside economic growth. Credit growth has broadly tracked nominal GDP, with cycles of acceleration and moderation. The mid-2000s saw rapid corporate lending, followed by a period of stress and rising non-performing assets (NPAs) in the early-to-mid 2010s. The subsequent clean-up—recognition of bad loans, recapitalization of PSBs, and the introduction of the IBC—strengthened balance sheets.

In recent years, growth has been driven by:

Retail lending (home loans, personal loans)

Digital payments (UPI ecosystem)

Improved asset quality and capital positions

Looking ahead, structural drivers such as rising incomes, formalization of the economy, and low credit penetration relative to GDP suggest sustained medium-term growth potential. However, growth will remain sensitive to interest rates, economic cycles, and global conditions.

India vs Global Banking Giants

Globally, the largest banks—such as JPMorgan Chase, Industrial and Commercial Bank of China (ICBC), and HSBC—operate at a scale far larger than Indian banks in terms of assets and international presence. These institutions benefit from deep capital markets, global operations, and diversified revenue streams.

Indian banks, while smaller in global rankings, compare favorably on certain dimensions:

Growth rates: Higher due to India’s emerging economy dynamics

Digital innovation: India’s payments infrastructure (UPI) is among the most advanced globally

Return potential: Private banks, in particular, have delivered strong return metrics over long periods

The key gap remains in scale and global reach, though India’s banks are steadily strengthening capital, governance, and technology capabilities.

Conclusion

The banking industry is a foundational pillar of the economy, quietly enabling everything from daily transactions to large-scale industrial growth. In India, the sector has evolved from state-led expansion to a more balanced ecosystem where public and private players coexist, regulated by a robust framework under the RBI.

As the economy formalizes and digitizes further, banks are likely to become even more central to financial intermediation. For observers and investors alike, understanding how banks work—how they earn, manage risk, and operate within regulation—provides valuable insight into the broader health and direction of the economy itself.